Increased Demand from Credit Managers Claiming GIPS Compliance

Claiming compliance with the Global Investment Performance Standards (GIPS®) is gaining significant traction with credit asset managers due to the increased demand from institutional investors.

Historically, only the largest credit asset managers have claimed compliance with the GIPS standards (63% of the top 40 CLO managers as ranked by Creditflux and reported in eVestment's consultant database). Today however, we are seeing a noticeable shift towards smaller managers inquiring about GIPS compliance. These credit asset managers oversee a variety of vehicles including CLOs, separately managed accounts investing in the credit market, credit hedge funds, private debt and distressed debt funds, direct lending products, BDCs, and others. We believe the trend towards GIPS compliance across the credit space will continue to grow as investors and allocators continue to request and require GIPS compliance from competing managers.

According to a recent Reuters article, “[t]here has been US$124.6bn of US CLOs raised this year through December 7, topping the previous record of US$123.6bn set in 2014, according to LPC Collateral data. Another US$149.6bn of deals have been refinanced, reset, or reissued in 2018.” This growth is not restricted to leveraged loan mandates but has expanded to private debt, emerging market debt, and other credit mandates as well.

Given the standardized calculation and presentation requirements, the GIPS standards should pair nicely with the growth in the asset class and help firms provide a deeper level of transparency for consultants and prospective clients to analyze and compare investment performance history. Included below is a list of institutional RFPs for credit-specific mandates issued over the last several months. Noteworthy is the fact that GIPS compliance, and sometimes verification, was required as a minimum criterion for consideration in each case.

| Investor | Date of Issuance/Deadline | Mandate Name | Mandate (Millions) | GIPS Compliance Requirement |

|---|---|---|---|---|

| LACERA | 4/5/2019 Issued | Syndicated Bank Loan Mandate | ~$500 | “Must comply with the Global Investment Performance Standards” Source – Note: RFP also requests a copy of Verification report |

| Louisiana Municipal Police Employees’ Retirement System (MPERS) | 4/5/2019 Issued | Intermediate -Term Investment Grade Fixed Income Mandate | $50 | “The track record must be calculated in full compliance with the CFA Institute’s Global Investment Performance Standards (GIPS).” Source |

| LACERS | 4/12/2019 Deadline | High Yield and Bank Loan Mandate | $50 | “The Proposer must have a minimum of five years of verifiable GIPS-compliant performance history actively managing the proposed product for institutional clients.” Source |

| LACERS | 12/10/2018 | Private Credit Mandate | $670 | “As outlined in the RFP, the submitted track record must conform to GIPS. There is no flexibility around the 5-year track record requirement.” Source |

| Louisiana Municipal Police Employees’ Retirement System (MPERS) | 5/28/2018 | High Yield Bond Mandate | $50 | “The track record must be calculated in full compliance with the CFA Institute’s Global Investment Performance Standards (GIPS).” Source |

| Cambridge Retirement Board | 3/7/2019 | Bank Loan Mandate | $35 | “The firm has at least 5 years of GIPS compliant investment performance.” Source |

| Policemen’s Annuity and Benefit Fund of Chicago | 5/31/2018 Deadline | Emerging Market Debt Mandate | $50 | “The firm should have a minimum 3 years of GIPS compliant performance as of March 31, 2018.” Source |

What do credit firms need to consider before claiming GIPS compliance?

There are several important focus areas that a firm should consider before claiming compliance with the GIPS standards.

The Common Issues

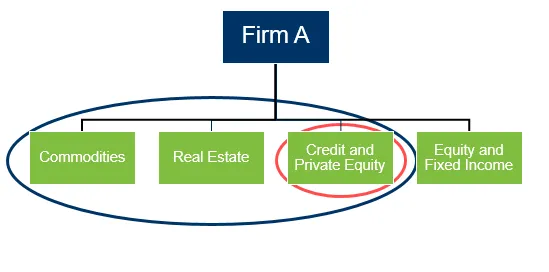

- Firm Definition – Provision 0.A.12 requires that, “firms must be defined as an investment firm, subsidiary, or division held out to clients or prospective clients as a distinct business entity.” For many firms, defining the GIPS-compliant firm will be easy, as the legal entity only has one business line. However, for larger firms that manage assets across multiple business lines, attaining GIPS compliance at the entity, or “parent” level, may not be practical.

Example: Firm A has four autonomous divisions that manage commodities, real estate, credit and private equity, and other traditional equity and fixed income products.

In this scenario, the firm has the following options:

- Define the firm to include all of Firm A;

- Define the firm as just the Credit division; or

- Define the firm as some combination of multiple divisions.

- Discretion – Discretion, as defined in the GIPS standards, is the ability of the firm to implement its intended strategy. The GIPS standards require that all fee-paying and discretionary portfolios be included in at least one composite. If a portfolio has a client-imposed restriction, it may be classified as non-discretionary and not be included in any composite. Such restrictions may include frequent or scheduled cash withdrawals, restrictions on purchasing certain securities or sectors, mandates for higher-than-normal cash balances, restrictions on purchasing new issues, and credit quality limitations, among others. Determining discretion for a credit manager can often be challenging. For example, a credit mandate may impose certain constraints on the portfolio, such as warrants. The key determination of discretion is whether these restrictions truly impede the ability of the PM to implement the defined investment strategy. Consider an investment objective for an account that is to invest in below investment-grade first lien corporate loans primarily for middle market companies. There are also restrictions on credit quality and issue types. If the PM can still meet the objective, then this portfolio will be discretionary. If, however, the PM has to get approvals for every single trade from the client, then the portfolio should be considered non-discretionary. It is important to note that contractual discretion, from a regulatory perspective, does not automatically translate into discretion for GIPS compliance purposes, and firms will need to establish a definition of discretion to be in the GIPS policies and procedures manual.

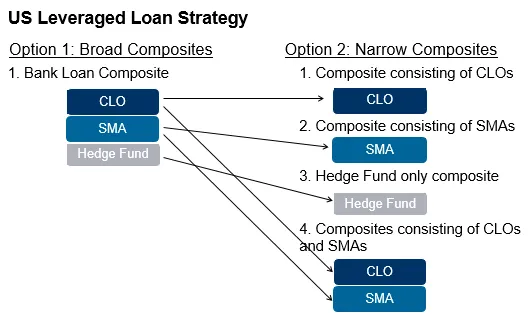

- Composite Construction – Provision 3.A.1 requires that, “all actual, fee-paying, discretionary portfolios must be included in at least one composite.” A composite is an aggregation of portfolios managed to a similar investment mandate, objective, or strategy. This has historically been a significant roadblock for credit firms when claiming compliance with the GIPS standards. When a credit manager oversees SMAs, private commitment-based funds, commingled funds, etc. it is often difficult to determine if the portfolios should be grouped together into a single composite or separated out based on portfolio type. In such a situation, it would be prudent to consider the firm’s marketing approach and how the portfolio type/composite dynamic is best approached. For example, cash flow restrictions in a fund may be very different from those in a SMA, and to combine the portfolios may distort the performance track record.

- Performance Calculations – The GIPS standards are mainly principles-based and allow for some flexibility to accommodate a given firm’s GIPS-compliant framework. There are, however, certain rules that all firms must adhere to.

- Currently, for most asset managers, the GIPS standards require firms to calculate portfolio performance by using a time-weighted return (TWR) methodology. However, there is relief allowed for portfolios defined as private equity or real estate equity. Given the nature of these vehicles, the industry standard is to calculate performance using a money-weighted return (MWR) (Note – TWR as well as MWR required for Real Estate). The upcoming release of the 2020 GIPS Standards in June 2019 should ease the challenges for credit managers somewhat, as firms will be able to determine if TWR or MWR is most appropriate, based on certain prescribed criteria – primarily, whether or not subscriptions and redemptions are controlled by the portfolio manager.

- Credit firms typically don’t have a system in place to properly calculate composite returns and therefore use Excel. In this case, it is important to document the process and methodology for calculating performance. If using Excel is not sustainable, then firms should consider looking into portfolio accounting and composite systems that have the ability to support such calculations.

- Marketing – Credit firms often ask whether current marketing efforts will be affected by a claim of GIPS compliance. As long as a firm claiming GIPS compliance has satisfied the obligation to provide a compliant presentation to all prospective clients at least once every twelve months, there is no reason to alter the marketing approach. Marketing materials must not, of course, be false or misleading and need appropriate disclosure.

Due to the recent increase in demand for GIPS compliance, primarily driven by institutional allocators, the GIPS standards have become an agenda item in many investment committee meetings. With the proper education, planning, and resources, GIPS compliance can be achieved in a reasonable timeframe. For firms that do not have in-house GIPS standards expertise, we recommend hiring an outside consultant/verifier that is knowledgeable, especially with applicability to credit managers. A gap analysis project will help firms understand any potential issues to be overcome to claim GIPS compliance. The gap analysis will also assist in the development of a roadmap by which the firm can allocate time and resources, should the firm decide that GIPS compliance is a worthwhile endeavor.

Resources

Watch our complimentary webcast: The Credit Manager’s Guide to GIPS Compliance highlighting the important areas that credit asset managers should understand as they consider or seek GIPS compliance.

ACA Performance Services assists many different credit managers in their efforts to claim compliance with the GIPS standards and ultimately become verified. If your firm is looking for more information into this effort, please contact Christie Dillard.

About the Author

Shivani Choudhary, CFA, CIPM, is a Senior Performance Consultant with ACA Performance Services, a division of ACA Compliance Group. Working from our Chicago office, Shivani manages a diverse client base of GIPS compliance verification engagements, as well as conducting performance certifications and focused reviews, for firms of all sizes and asset classes. Prior to joining ACA, Shivani worked for Guggenheim Partners Investment Management as a senior performance measurement associate. Shivani earned her Masters of Business Administration (MBA) (Finance emphasis) from the Illinois Institute of Technology and her Bachelor of Science in Engineering (Electronics and Instrumentation) from the Institute of Technology and Management in India. She also has earned a Certificate in Investment Performance Management (CIPM) from the CFA Institute and is a CFA Charterholder.

Related insights

Your Guide to a Compliance Testing Action Plan

Maintaining a strong compliance program requires regular testing. Download our plan to ensure robust testing.

- Compliance

- Cybersecurity

- Performance

- Portfolio Company Risk Management

- Privacy

- Trade Surveillance

SEC Marketing Rule FAQs for Gross and Net Performance of Extracted Performance

The FAQ clarifies how to show gross and net performance of extracted performance and performance characteristics.

- Performance

- Compliance

- SEC Marketing Rule

- SEC

Countdown for OCIO Portfolios to Comply with the GIPS Standards Newest Guidance Statement

The new requirements become effective December 31, 2025. We’ve created a template timeline to guide your firm towards full compliance by the end of the year.

- Performance

- GIPS Standards